A written approval letter provides you with the leverage you need to obtain the very best price and terms. In a competitive situation, you gain an advantage with a strong approval letter.

The Benefits of an Approval Letter:

Important to keep in mind: What you are qualified to pay versus what you are comfortable paying for a monthly mortgage payment may be two different numbers. You can often be approved for a much larger monthly payment than what you will actually be comfortable paying each month- this is something to discuss with your lender or your Realtor. A good Realtor will respect those boundaries regardless of what the numbers say you can afford. Do not let anyone convince you to look “just a little bit higher”.

The seller expects your financing to be approved prior to submitting an offer. Anything less will put you at a competitive disadvantage at contract time.

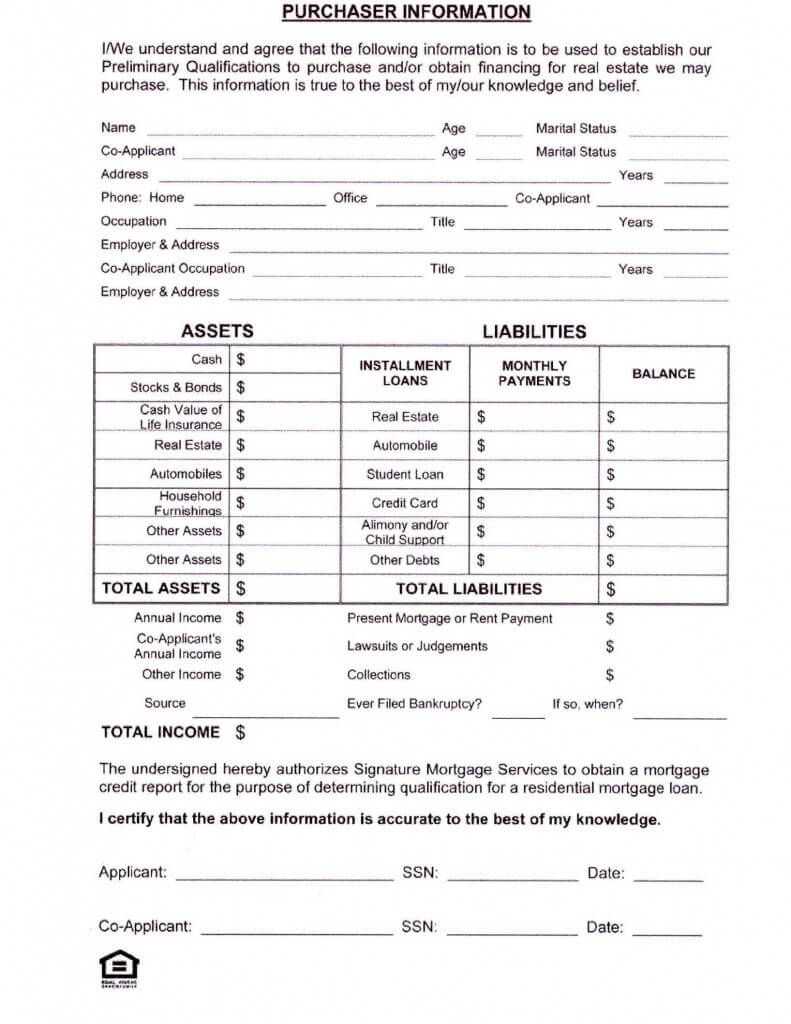

There are several documents that may be required by the lender in order to issue a commitment or pre-approval letter.

This list may look daunting at first glance, but many of these items are easily available with a quick trip to your lending institution and a look over your old tax forms. Your lender will help walk you through the document collection process.

Pre-Approval means that you have made written loan application with documentation and it has been approved by the lender.

Pre-Qualification means only that a conversation with the lender has taken place but nothing has been verified and no commitment has been made by the lender.

When your full loan application and documentation has been reviewed by the lender’s underwriter and approved, you will receive a commitment letter. Conditions for funding the loan after this lender commitment is made typically include:

In addition to the amount of the loan, these are some costs that you should expect to provide at closing. *All numbers used are for example purposes but are reflective of actual costs for a similarly priced home.

| To vendor on closing: | $149,000 |

| Mortgage Amount: | ($100,000) |

| Legal fees | $0.00 |

| HST 13% | $0.00 |

| Search Costs | $160.19 | Fax transmissions | $15 |

| Executions Certificate | $34.50 | Couriers | $45 |

| Subsearch | $34.31 | Long distance phone | $5 |

| Photocopies | $50.00 | Miscellaneous Expense | $50 |

| Postage | $15 | Software Transaction Charge | $20 |

| E-Reg service charge | $25 | ||

| Total: | $454 |

| Title Insurance Premium | $282.00 |

| Registration of Transfer | $74.,72 |

| Registration of Charge | $74.72 |

| Ontario Land Transfer tax | $1,225.00 |

| Total: | $1,656.44 |

Total Legal Fees, Disbursements and HST: $2,169.46

Client to bring certified cheque payable to Lawyer,

In trust, in the amount of: $51,279.35

If you are concerned about not being able to cover the funds needed at closing, there are several things that we can do to negotiate these so that the seller can pay them or they can be tied into your loan.

Obtaining hazard/homeowner’s insurance used to take a matter of minutes- now it can take days or even weeks. Because of a string of weather-related losses and many other factors, hazard insurance is now more expensive and it takes longer to get.

Insurance underwriters not only look at the claims history of the current homeowner and specific property; it is highly likely that they will also be evaluating your own claims history as well. Therefore, it is critically important to initiate the process of getting hazard insurance before we have even identified the home you wish to purchase. Getting started on this process is as important as getting your mortgage.

I strongly recommend that you call your current insurance company or insurance broker right away. Bear in mind that the length of time you have been a customer of a particular insurer or the amount of business you do with them does not mean as much as it used to, and the underwriting guidelines that insurers use change on an almost daily basis.

Please do not leave this important task to the last minute. Unless you are purchasing a condominium, closing will most likely not be able to occur until you have proof of homeowner’s insurance.

In today’s market, it is critical to begin the process of obtaining hazard insurance as soon as you have a ratified contract.Under no circumstances should you leave this to the last minute.

Your lender requires that you keep the property insured against damage or destruction and name them as the co-insured. This is referred to as hazard insurance.

Homeowner’s Insurance is hazard insurance plus liability and contents coverage for the owner. Almost without exception, purchasers obtain Homeowner’s Insurance. Your policy must be paid for and a binder issued prior to closing. Evidence of such must be delivered to the lender prior to funding the loan.

For Condominium Purchasers: The master policy covers the structure of the building on behalf of you and your lender and is paid for in your condo fees. However, this provides no liability and contents coverage for you, and no coverage if another unit is damaged by something that occurs within your unit. Please speak with your insurance agent to discuss adequate separate coverage for your personal belongings.